What is the ATO Disclosure of Business Debts legislation

Businesses are responsible for ensuring tax and superannuation obligations are reported and paid on time. The purpose of the ATO Disclosure of Business Debts legislation is to encourage businesses to engage with them to manage tax debts, support them to make more informed decisions, and reduce the unfair advantage of businesses that do not pay on time.

The ATO may disclose overdue business tax debt to approved credit reporting bureaus (including Access Intell) if a business meets the following criteria:

- The business has an Australian business number (ABN) and is not an excluded entity.

- The business has one or more tax debts and at least $100,000 is overdue by more than 90 days.

- The business is not engaging with the ATO to manage their tax debt.

Why ATO tax default data is important for credit managers

Visibility of overdue tax debts helps businesses to make more informed decisions about who to trade with and whether to extend trade credit.

Post-Covid, the ATO has returned to business-as-usual debt collection activities. This included the disclosure of over 36,000 business tax debts in the 2023-24 financial year.

Businesses able to access tax debt information receive early warning of possible distress in the defaulting customer allowing them to manage their risk exposure and proactively work with affected customers.

How do Director Penalty Notices relate to ATO tax default data

If a company does not pay certain tax liabilities by the due date, the ATO can issue a Director Penalty Notice (DPN) to recover amounts due by the company personally from current or former company directors.

Once a DPN is issued, a director has 21 days to act before they become personally liable. Options typically are to pay the debt or appoint an Insolvency or Small Business Restructuring Practitioner.

Insolvencies are at a historical high, with the popularity of small business restructuring (SBRs) continuing to increase, usually in direct response to ATO debts. Alares data shows a continued year-on-year increase in ATO-initiated Court recoveries. According to Insolvency Australia’s most recent Corporate Insolvency Index, there has been a three-fold increase in SBRs in the first half of the 2025 financial year.

DPNs continue to ramp up post-COVID, as the ATO focuses collection efforts on businesses that refuse to engage using effective tools like DPNs and garnishees.

In 2023–24, 26,702 DPNs were issued for company debts totalling over $4.4 billion – with approximately $879 million collected as of 30 June 2024. An additional 8,714 DPNs were issued to individual directors of 6,493 companies, for $572.7 million in unpaid super guarantee, with $483.6 million remaining outstanding.

How to access ATO tax default data

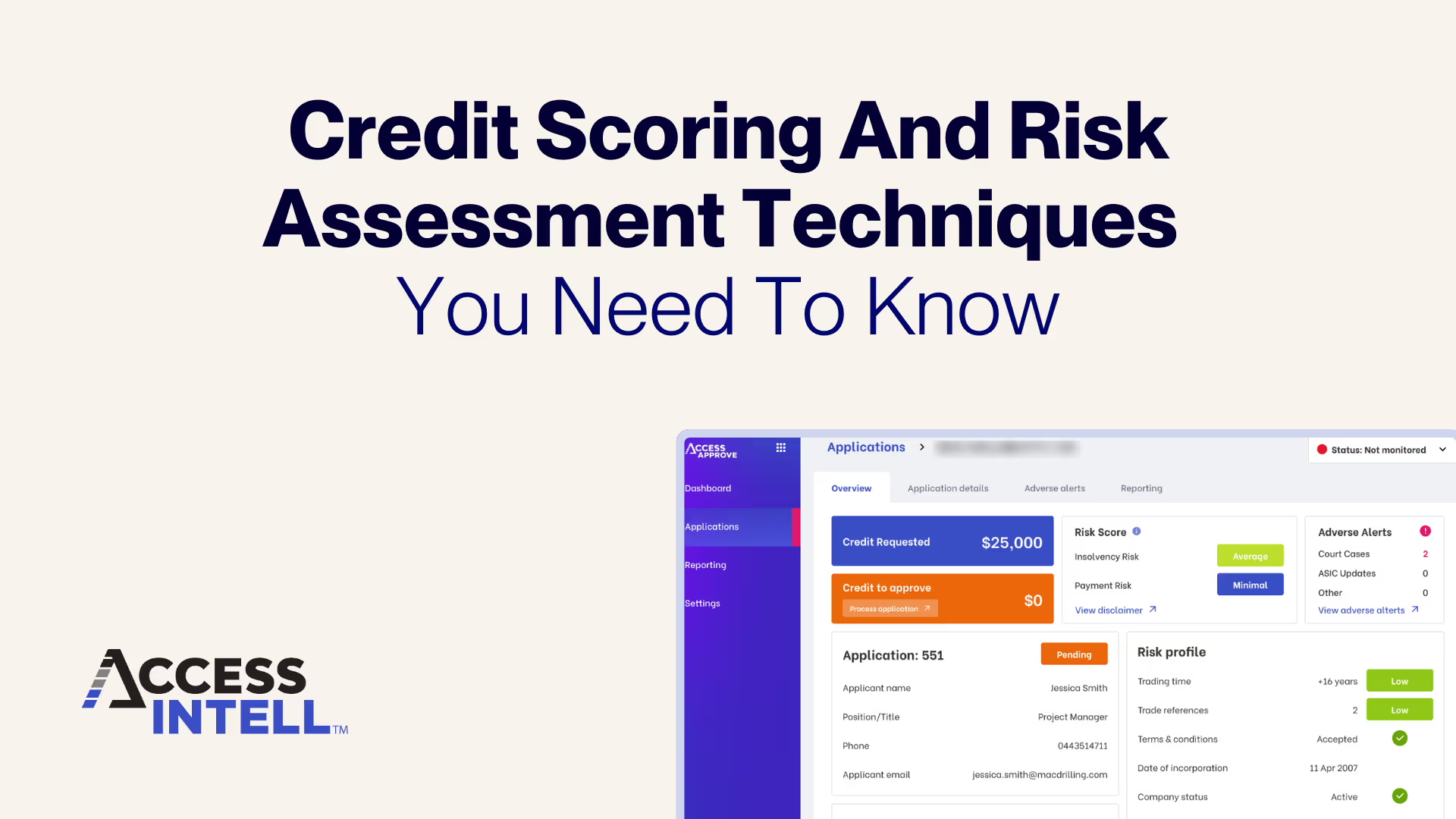

The ATO discloses the tax default data to approved credit reporting bureaus, including Access Intell. Clients that use our online trade application and assessment and credit risk monitoring products have instant access to this vital information both within the platform and via email alerts.

Key Takeaway

Credit Managers should think of disclosed tax debts as a red flag alert. Depending on risk appetite, it may help you decide whether to offer a cash account rather than extending credit. Using this data proactively can mean the difference between suffering a large bad debt and protecting your business.

Want to receive alerts when your customers have reportable ATO business tax debts? Ask us about Access Monitor today.