Quick Facts

- Shifts overdue tax liability from company to directors personally

- 21-day rule for directors to act

- $4.4 billion in company tax debt pursued via DPNs in 2023‑24 (ATO 2023‑24 Annual Report)

- 84,529 DPNs issued in 2024-25 to individual directors in respect of liabilities of $5.5 billion (ATO 2024-25 Annual Report)

What is a Director Penalty Notice (DPN)?

A DPN is issued by the ATO to recover overdue tax liabilities by a company personally from current or former company directors. These tax liabilities include unpaid Business Activity Statements (BAS) or Superannuation Guarantee Charge (SGC) or Instalment Activity Statement (IAS).

There are two types of DPNs:

- Non-Lockdown (21 Day) DPN: Issued when returns have been lodged on time, but the debts remain unpaid. Directors have 21 days to act before they become personally liable. Options typically are to pay the debt or appoint an Insolvency or Small Business Restructuring Practitioner.

- Lockdown DPN: Issued when returns are lodged late or not at all. Directors are ‘locked’ into personal liability immediately, with no option to avoid the liability through actions like restructuring.

ATO director penalty notice (DPN) rates

DPNs continue to ramp up post-COVID, as the ATO focuses collection efforts on businesses that refuse to engage (ATO debt‑collection posture update, Oct 2024). In 2023–24, 26,702 DPNs were issued for company debts totalling over $4.4 billion – with approximately $879 million collected as of 30 June 2024 (ATO 2023‑24 Annual Report). An additional 8,714 DPNs were issued to individual directors of 6,493 companies, for $572.7 million in unpaid super guarantee, with $483.6 million remaining outstanding (ATO 2023‑24 Annual Report).

How are DPNs Driving Insolvencies?

Insolvencies are at a historical high (ASIC Insolvency Statistics, as at June 2025). The popularity of Small Business Restructuring (SBR) continues to increase, usually in direct response to ATO debts and subsequent DPNs (ABC News, July 2025).

ASIC data shows a significantly growing uptake in SBRs, from 448 appointments in 2022–23 compared to 1,425 in 2023–24, with the number of appointments for 2024–25 projected to be ≈3,000 (ASIC Review of small business restructuring process: 2022–24).

Additionally, data shows a continued year-on-year increase in ATO-initiated Court recoveries.

The 21‑day window is frequently a trigger for directors to appoint an external administrator (ATO Director Penalty Regime). This leads to insolvencies or SBRs seemingly coming ‘out of the blue’ to creditors.

What does a director penalty notice mean for creditors?

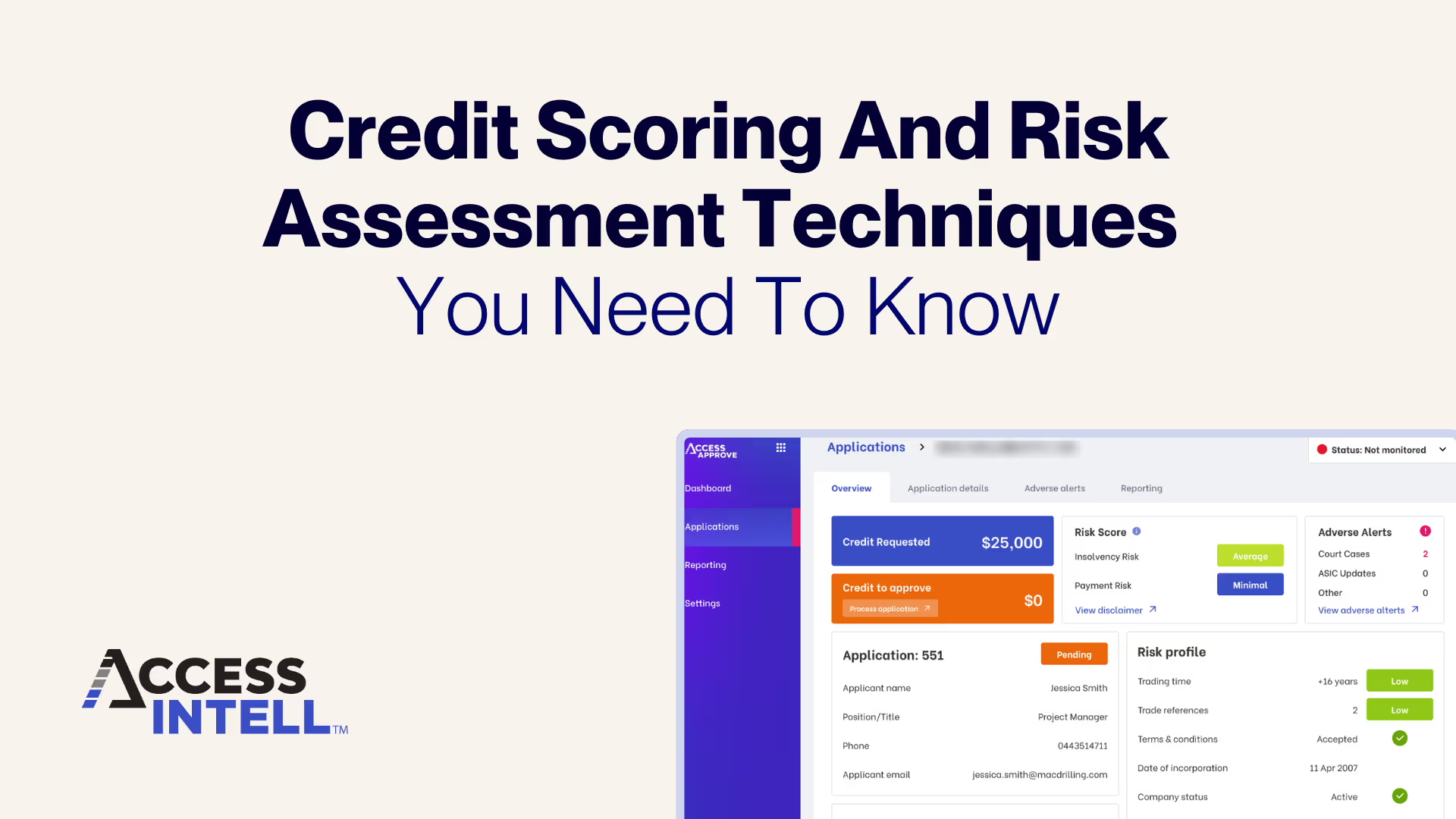

The ATO may disclose overdue business tax debt to approved credit reporting bureaus (including Access Intell) if a business meets certain criteria. An ATO business tax debt default is a leading indicator of a DPN and/or a business entering an SBR. Companies subject to ATO reporting having a very high failure rate. Strong credit management and proactive risk monitoring can surface red flags including this. Clients that use our online trade application and assessment and credit risk monitoring products have instant access to this vital information both within the platform and via email alerts.

Using this data proactively can mean the difference between suffering a large bad debt and protecting your business.

Key Takeaway

DPNs are usually a symptom of deeper customer financial issues and are a key driver of small business restructuring and insolvencies. Be alerted to signs of risk by continuously monitoring your customers with Access Intell.