What is a credit policy?

A credit policy is a formal document that outlines your company’s approach to granting credit, setting terms and managing overdue accounts. It acts as a roadmap for your credit team, ensuring decisions are based on clear, consistent criteria.

Why Is It Important?

- Reduces risk: Helps you avoid extending credit to high-risk customers.

- Improves cash flow: Encourages timely payments and reduces overdue accounts.

- Supports compliance: Ensures your business meets legal and regulatory requirements.

- Builds trust: Customers appreciate transparency and clear expectations.

Why a credit policy matters

A well-structured credit policy is the backbone of effective credit management for businesses large and small. It sets clear expectations for customers, reduces bad debt and ensures consistency across your business. Without one, you risk inconsistent decisions, increased exposure to insolvency, and strained customer relationships.

Key Elements of an Effective Credit Policy

When drafting your credit policy, include these essential sections:

Credit Assessment Criteria

Define how you evaluate a customer’s creditworthiness. This may include:

- Financial statements

- Credit reports

- Payment history

- Industry risk factors

Credit Limits and Terms

Specify:

- Maximum credit limits

- Standard payment terms (e.g. 30 days)

- Conditions for exceptions

Documentation Requirements

Outline what documents are needed before extending credit, such as:

- Signed terms and conditions

- Personal or director guarantees

- Purchase orders

- When a PPSR registration should be made

Collection Procedures

Detail the specific steps for overdue accounts:

- Reminder notices (these can be automated through your accounting software)

- Escalation process

- Legal action if necessary

Review and Update Schedule

Set a timeline for regular reviews, at least annually or when market conditions change.

Practical Tips for Credit Managers

- Keep it clear and accessible: Avoid jargon. Your policy should be easy for staff and customers to understand.

- Align with business goals: Ensure your credit terms support sales objectives without compromising risk management.

- Train your team: A policy is only effective if everyone follows it. Provide training and resources.

- Use data to drive decisions: Base credit limits and approvals on accurate, up-to-date information.

How Access Intell Can Help

Access Intell offers powerful tools to make implementing and managing your credit policy easier:

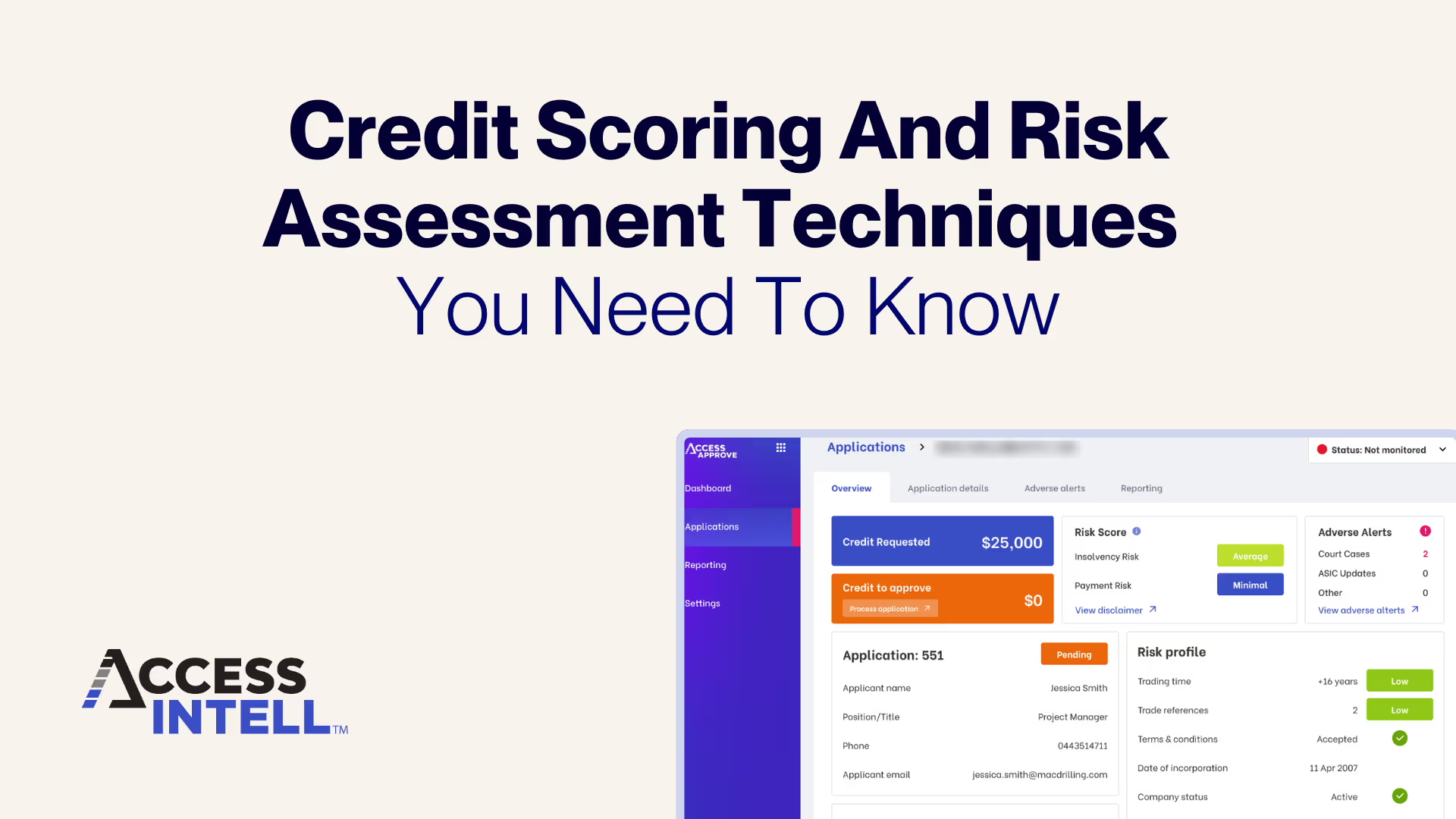

- Credit risk assessment: Instantly access business creditworthiness data and adverse alerts to evaluate customers before granting credit.

- Centralised PPSR: Manage PPSR registrations with our centralised, automated software to ensure accurate protection.

- Automated monitoring: Receive real-time notifications of changes in a customer’s financial status, helping you act quickly.

- Multi-bureau credit reports: Generate detailed credit reports from your choice of bureau to support your policy decisions and audits.

- Integration with your workflow: Our solutions fit seamlessly into your existing processes, saving time and reducing manual errors.

An effective credit policy protects your business and strengthens customer relationships. By combining clear guidelines with smart technology, you can minimise risk and maximise efficiency.